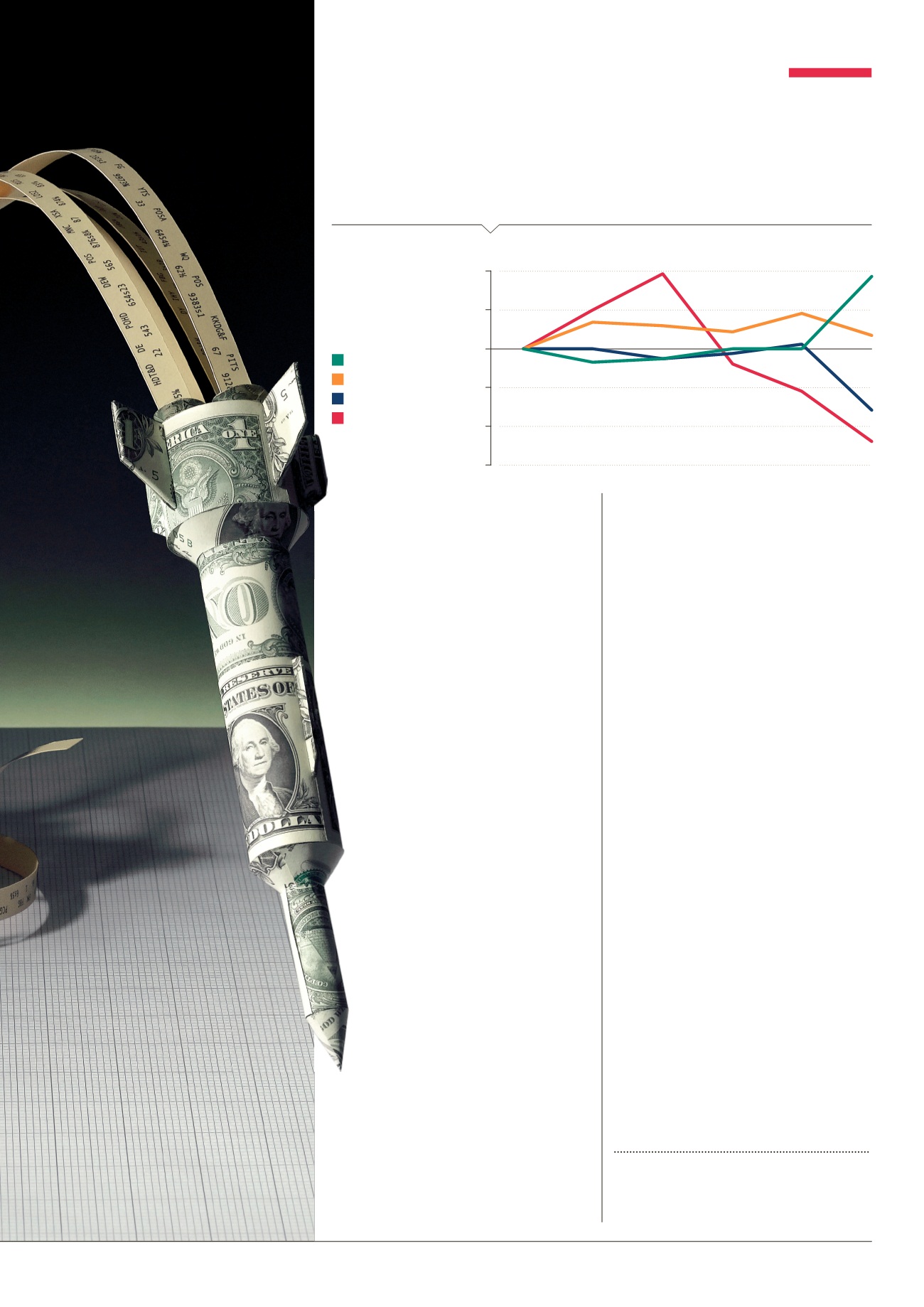

US dollar

British pound

Euro

Japanese yen

HOW CURRENCY

STRENGTH HAS

CHANGED OVER

THE PAST FIVE YEARS

(BASED ON 19 MARCH,

2010 SPOT RATE)

THE INVESTOR

|

17

appreciation of the dollar,’ says former Bank

of England rate-setter professor Charles

Goodhart. But he sees‘sterling’s usual

position midway between the US dollar and

the euro as not entirely comfortable, since

most imported commodities are priced in

dollars and most exports go to Europe’.

That means the UK is at risk of losing

competitiveness, squeezed between an

appreciating dollar and a depreciating euro.

The problem is compounded for smaller

countries trying to maintain a currency

peg – where one country’s exchange rate

with another is xed – with larger trading

partners. Switzerland has long been treated

as a‘safe haven’. Since its main trading

partner is the eurozone, it decided to peg

the Swiss franc to the euro. But the euro’s

sharp depreciation in 2014 triggered

massive in ows into Switzerland, putting

upward pressure on its currency.When its

central bank unexpectedly abandoned the

peg, the Swiss franc’s value jumped by 20%,

leaving the country’s exporters facing some

hard choices.

Since then the pressure has shifted to

Denmark, whose currency is also pegged

to the euro.‘Denmark’s situation is very

dangerous,’ says professor Philip Booth

of City University’s Cass Business School.

‘It is similar to that of the UK when we

were shadowing the Deutschmark in the

early Nineties.’ Its central bank has moved to

negative interest rates – e ectively charging

investors for the privilege of holding krone.

But for speculators seeking large currency

gains when the peg is abandoned, this looks

like a one-way bet.

‘Small economies don’t have to peg,’ says

De Grauwe, adding that countries‘like Sweden

and Norway, which have maintained exible

exchange rates, have been relatively successful’.

But Sweden has had to reverse its policy

of raising interest rates to head o a property

bubble precisely because this had caused its

currency to rise too far.

Booth believes that in the past‘ oating

exchange rates have served very well in dealing

with major nancial shocks’.The greatest

threat of currency wars may be in the Far

East where Japan has embarked on the most

extreme form of stimulus tried so far in order

to jolt its economy out of two decades of

stagnation.‘The short-term e ect has been to

reduce the value of the yen, but there is as yet

not much sign of it boosting economic growth,’

says Booth.

A weaker yen has made Japanese exports

more competitive, but that is putting pressure

on major trading partners. Should China

take retaliatory action and further loosen its

monetary policy, Booth believes this would

most likely raise internal prices in Japan and

o set any bene t of having a weaker currency.

So the end result is that – except for gaining

temporary competitive advantage – nobody

really wins from currency wars. But currency

wars mean interest rates will probably stay

lower for longer, forcing investors further up

the risk spectrum and fuelling asset prices.

Herein lie the real dangers.

ANALYSIS

Balance sheet

‘Unconventional measures’, used by

central bankers to combat weak growth and the threat

of deflation, mean that accusations of exchange rate

manipulation have multiplied.

March

2011

0%

March

2012

March

2013

March

2014

March

2015

10%

20%

-30%

-20%

-10%

Source: Oanda.com

THE UPS AND DOWNS OF CURRENCIES

March

2010