THE INVESTOR

|

15

Anthony Hilton

is the financial editor of the

Evening

Standard

and former editor of

Accountancy Age

. He has

worked for

The Observer

, the

Daily Mail

and the

Sunday

Express

, and was business correspondent for the

Sunday

Times

in New York for three years.

which would see their solvency positions

dramatically improved because their

actuaries would be able to sign o on higher

future returns on their existing assets.

That would lift a nancial millstone from

companies and leave them with more cash

to invest and grow.And at an individual

level higher rates would feed through

immediately into higher annuity rates,

which could make a big di erence in the

future living standards of those with private

pensions who are soon to retire.

Above all, investors around the world

would be able to go back to making

decisions on what they see as the merits

of an investment – rather than trying to

second-guess the thinking and actions of

central bankers (which is, of course, what

ANALYSIS

Central bankers

understand the risks

of moving too fast

near historic levels – if there is going to be

an earthquake we can take comfort from it

being a small one.

It’s a shrewd strategy. Markets don’t like

uncertainty but the interest rate outlook is

no longer really uncertain.True, we don’t

know precisely when rates will go up, but

having been softened up for so long, surely

no one could claim it has come as a surprise

when it does happen. It is perfectly rational

to make investment decisions now which

position portfolios for the rate moves we

all expect in the coming months.This is

particularly the case in bond markets, where

rising interest rates unavoidably result in

a fall in capital values.

There will be pain elsewhere, too.

Household incomes have been squeezed for

a long time and, for some, an increase in

mortgage rates will be hard to take. Likewise,

some companies which would otherwise have

gone bust, have been kept a oat by cheap

loans – as shown by historically low levels of

bankruptcy.They will nd it much tougher in

normal times.

But the fear of dislocation should not stop

us from welcoming a world in which interest

rates are no longer arti cially low. Savers

have borne the cost of the global nancial

crisis for far too long and have had to endure

wafer-thin returns.A rate rise would be

even more bene cial for pension schemes,

investors should always do).The interest

rate is the market price for money; market

prices determine the allocation of resources.

We have lived for seven years with a

fundamental distortion of the economic

price mechanism; and even if we have

grown used to it we should not forget that

it is a distortion – and ‘normal’ is what we

should strive for. Indeed, though there may

be casualties and noise in the markets, we

should remember the words of US president

Franklin D Roosevelt in the 1930s that ‘the

only thing we have to fear is fear itself’.

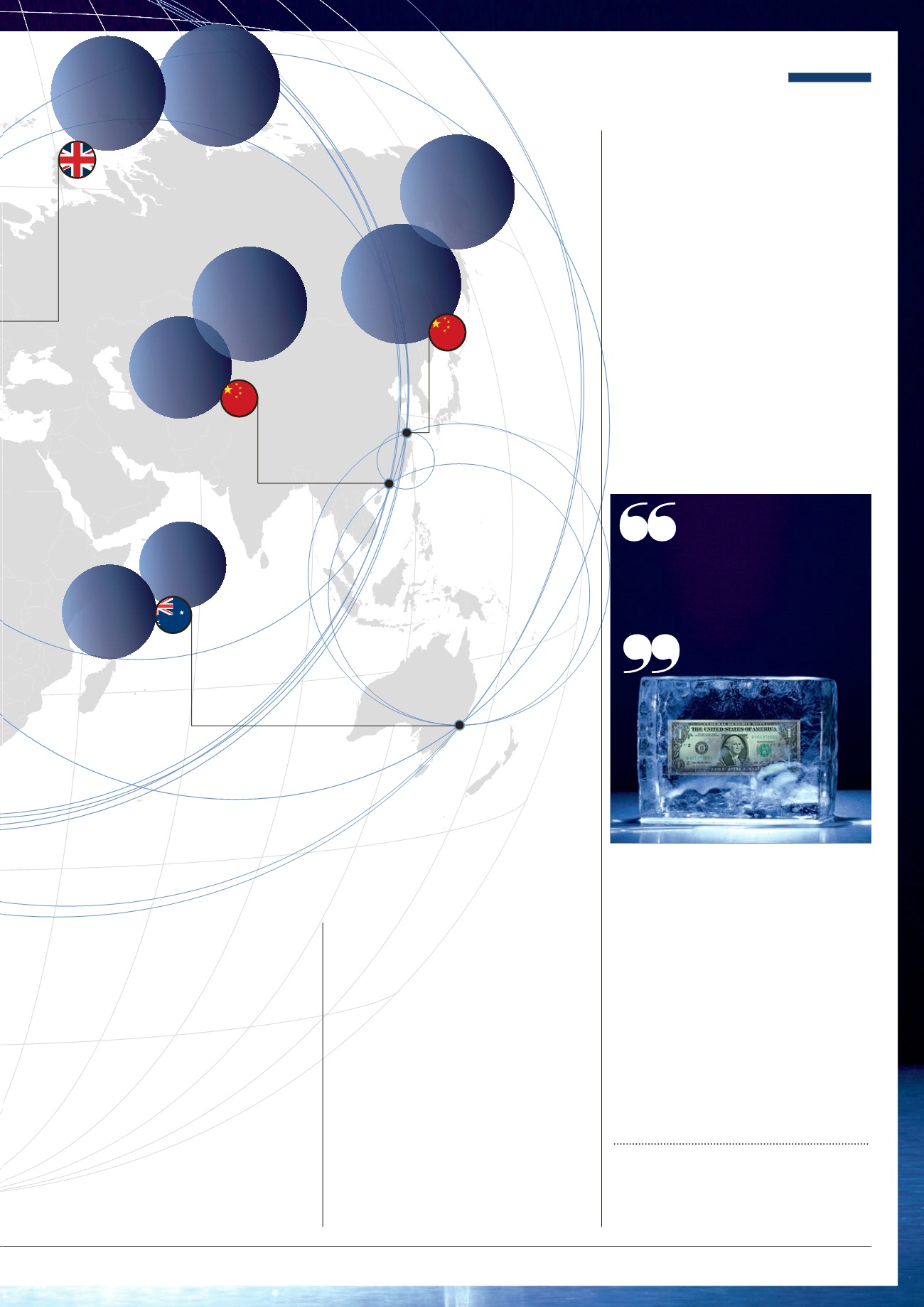

£4.36trn

market

capitalisation

Stock exchange

in the UK and

the largest

in Europe

LONDON STOCK

EXCHANGE

AUSTRALIAN

SECURITIES EXCHANGE

listed companies

and issuers

2,200

AUS

$1.5trn

market

capitalisation

$4.4trn

market

capitalisation

SHENZHEN

STOCK EXCHANGE

$5.9trn

market

capitalisation

SHANGHAI

STOCK EXCHANGE

Shenzhen is

the world’s

best-performing

market

this year

Topped the

5,000

level in early June

for the first time in

seven years