38 / 40

38 / 40

di erent aims than a company simply

seeking to survive, compete and grow.

Instead, company priorities may include

increasing employment or national

GDP growth, or even enabling

corrupt practices.

Finegan’s conservatismmeans that

balance sheet sustainability is an

important part of his thinking. It was the

di erentiating factor when he was

evaluating Shoprite, a SouthAfrican

supermarket operator, and BhartiAirtel,

an Indian telecoms company, who have

INSIGHTS

38

|

THE INVESTOR

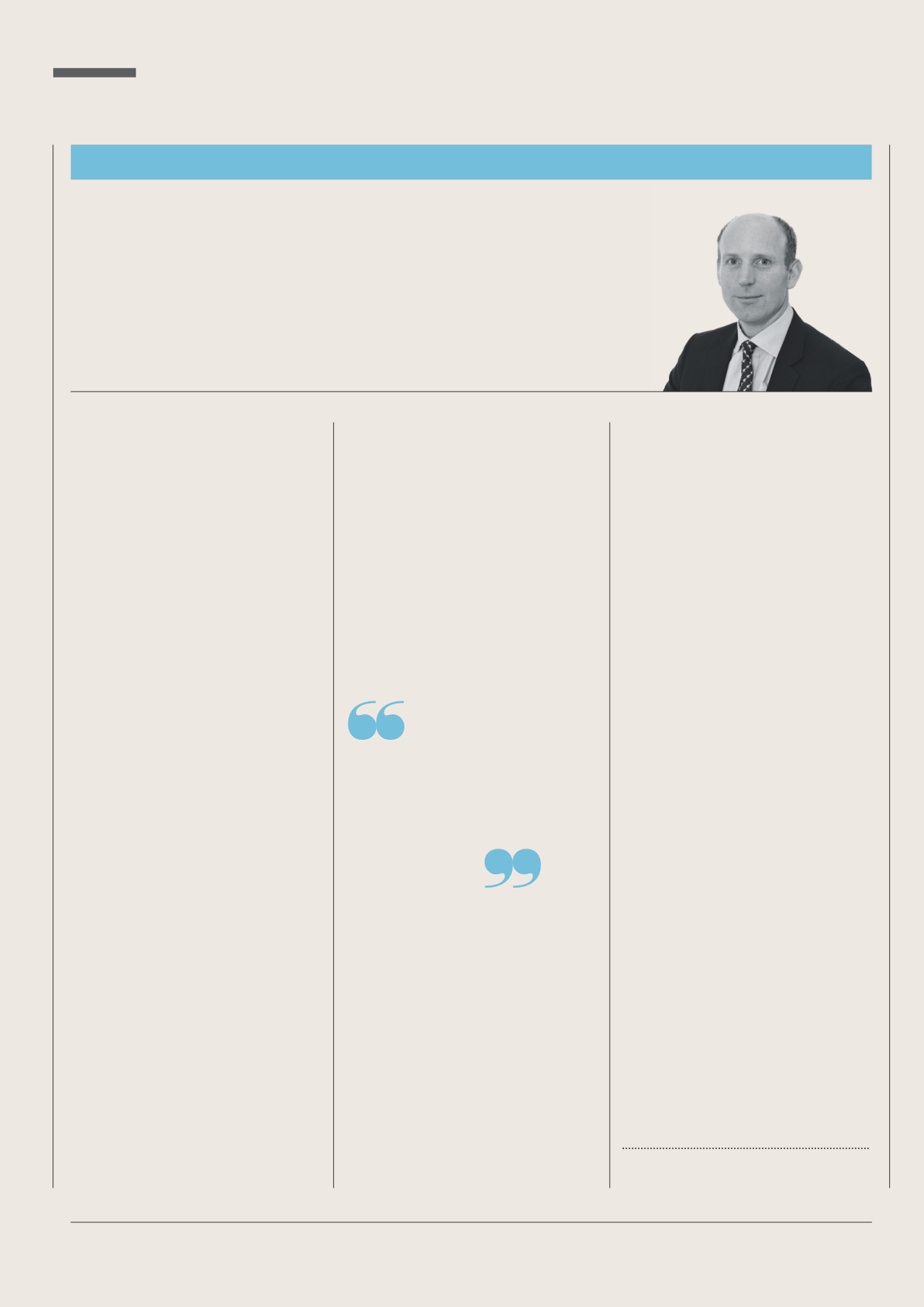

Glen Finegan of Henderson Global Investors

believes emerging markets pose specific risks to

investors – and knowing local practices is key

Most of the

companies we look

at have a controlling

shareholder

THE INVESTOR CENTRE

E

quity investors can have a

reputation for bullishness,

and all the more so when

their focus is emerging

markets. But Glen Finegan

is keener to emphasise the challenges.

“You win in emerging markets by not

losing,” says Finegan. “Go in with your

eyes open.There are risks everywhere.”

Manager of the St. James’s Place

Global Emerging Markets fund, Finegan

argues that emerging markets come

with their own problems.Many of the

usual rules (and laws) do not apply.

“Most of the companies we look at

have a controlling shareholder,” says

Finegan. “If they wish to prevent us

bene ting from the success of their

business, there is little we can do – for

example, going to court in Moscow

against an oligarch is very di cult.”

While population sizes in developed

countries have largely stagnated, numbers

in developing markets are still rising, and

are forecast to continue doing so over the

next three decades. But he thinks

emerging market indices are misleading,

since they re ect the weighting of the

companies within them– and the biggest

are often too politicised to operate as

ordinary companies.

“Many of these enterprises are not

really businesses at all,” says Finegan.

“A Chinese state-controlled bank is an

extension of the Ministry of Finance.”

Such companies are often run by

bureaucrats and their direction re ects

Emergingexpertise

about how they’ve been delivered,” says

Finegan. “I’d prefer a company with a

good record that’s been delivered in a

conservative manner.Many companies

in the portfolio don’t have any debt.”

Indeed, debt can be a particular

problem for companies in emerging

markets. The Nigerian naira began life at

parity with the dollar in 1973, but today

you need over 300 naira to buy $1.

“If you invest in a company in Nigeria,

you want to be certain its cash ows

will increase faster than in ation,” says

Finegan. “Fortunately there are some

[companies like that]. Heineken’s

subsidiary, Nigeria Breweries, owns the

strongest brewery in Nigeria. Its strong

brand has given it pricing power.”

Finegan spends a great deal of time

looking at a company’s controlling

shareholders, whether that’s a family,

founder or entrepreneur. He’ll study

how they’ve treated both shareholders

and other stakeholders in the business.

In these areas, he argues, virtue can

often signal a healthy sensitivity to risk.

“Do they try to avoid paying tax?

Are they content with their operations

polluting the drinking water for other

communities? Have they got a poor social

or environmental record?” he says.

“We can infer something about the

riskiness of the business if they don’t take

those issues seriously.”

both invested signi cantly in new

African markets.

“Shoprite has executed a risky

strategy in a conservative fashion – it’s

never geared its balance sheet,” says

Finegan. “Contrast that with Bharti

Airtel inAfrica, which borrowed in

US dollars and su ered as a result.”

In evaluating individual companies,

Finegan sets great store by its culture and

he spends longer studying a company’s

history than forecasting its future.

“We like companies with strong

nancial track records, but we care

This was originally published on Insights, available

via Partners’ websites or at www.sjpinsights.co.uk