19 / 40

19 / 40

THE INVESTOR

|

19

ISAs

Getty Images. Sources: 1 isaco.co.uk, May 2016; 2 gov.uk, April 2016; 3,4 royallondon.com, January 2017; 5,6 moneysavingexpert.com, April 2017

There are two variants of the

popular basic ISA – Cash and

Stocks & Shares. Around 80% of ISA

subscribers have chosen the cash

version

2

, but the combination of

stubborn inflation and record low

interest rates has resulted in even

these tax-advantaged savers suffering

negative real returns.

There is little light at the end of

the tunnel, as interest rates look set

to remain lower for longer given the

political and economic uncertainties

3

.

It means that billions in Cash ISAs is

failing to achieve the basic objective

of keeping pace with inflation.

Furthermore, the long-term trend

for favouring cash makes it clear

that ISA accounts are not being used

purely as a home for short-term

emergency funds, but are a key part

of the longer-term savings strategy

for millions of people; a problem that

could become worse with the advent

of the Lifetime ISA.

A report by mutual insurer Royal

London estimates that Cash ISA

savers have already missed out on

more than £100 billion in tax-free

gains that they could have made

over the past 10 years by investing

in a well-diversified Stocks & Shares

ISA

4

. The net result is that many more

people will find in later life that their

savings have shrunk in real terms.

The introduction of the Personal

Savings Allowance in April 2016 has

raised further questions over the

use of ISAs as a home for cash. This

makes interest earned on all standard

current and savings accounts tax-free

up to a limit of £1,000 a year for

basic-rate taxpayers and £500 for

higher-rate taxpayers

5

.

At current average savings rates,

a basic-rate taxpayer would need

savings in excess of £256,000

before paying tax on their interest,

and a higher-rate taxpayer just over

£128,000

6

.

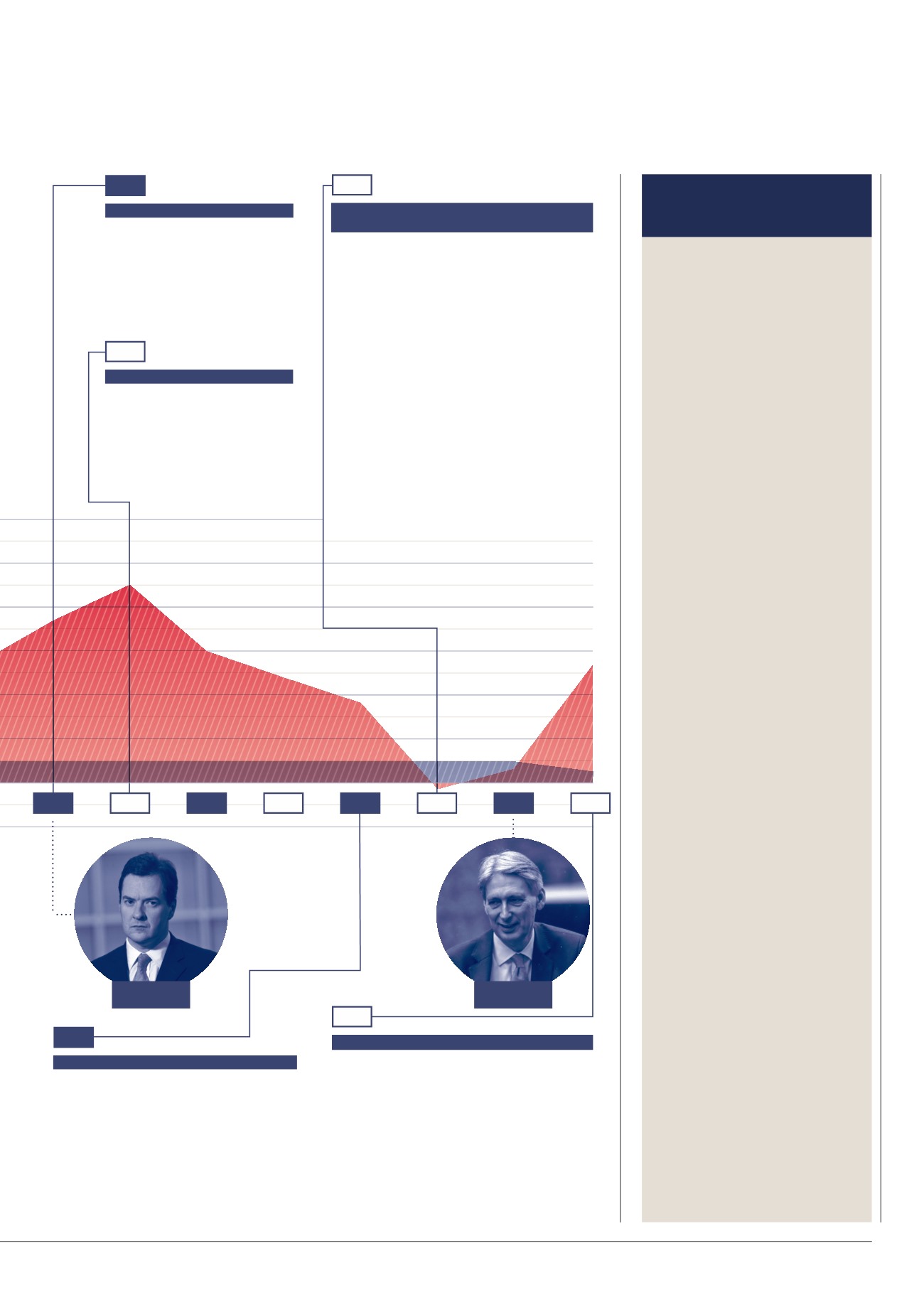

CASH ISAs – THE REAL

DEAL?

MORE FLEXIBILITY AND HELP FOR

FIRST-TIME BUYERS

ISA RULES TWEAKED

JUNIOR ISA

INFLATION LINKING

HELLO, LISA

2015

2014

2017

2011

2010

2010

2011

2016

2012

2017

2013

The

Flexible ISA

gives savers freedom to take

money out of an ISA and reinvest it later in the

same year and the limit rises to £15,240. In

addition, the

Help to Buy ISA

arrives. For every

£200 someone saves in the account for their

first home, the government adds £50 up to

a maximum bonus of £3,000.

Osborne announces that a new Personal

Savings Allowance will make returns on any

standard current and savings accounts tax-free,

up to a limit of £500 a year for higher rate

taxpayers and £1,000 a year for basic rate

taxpayers. This calls into question the value

of standard Cash ISAs’ unique tax-efficient

status of savers well within these limits.

Conservative Chancellor George Osborne

overhauls the ISA rules. The new ISA

allowance jumps to £15,000 and can be

split between cash and stocks and shares.

The Junior ISA limit climbs to £4,000. In

a surprise move, Osborne announces the

Inheritance ISA

, which allows widows and

widowers to inherit ISA funds tax-free.

The

Junior ISA

is launched. Each

child can hold two accounts: one

Cash

and one

Stocks & Shares

,

with a total yearly limit of £3,600.

The Chancellor announces that

the annual ISA limit will rise in line

with inflation by tracking the retail

price index.

Chancellor Philip Hammond ushers in the

Lifetime ISA

(LISA) for those aged 18 to 40,

announced by Osborne the previous year. Up

to £4,000 can be saved each year with the

government adding a 25% bonus. Funds must

be used to buy a first home, otherwise they

remain in the account until the holder is aged 60.

Meanwhile, the individual ISA allowance for the

2017/18 financial year has risen to £20,000.

George

Osborne

Philip

Hammond

2015

2014