08

|

THE INVESTOR

ANALYSIS

UK ECONOMY

Gallery Stock, PA Photos

Whereas the US

imposed a lot of fiscal

austerity last year,

in the UKwe

front-loaded it

rise in wages until relative slack in the

labour market is taken up, when temporary

or part-time workers move into full

employment.’

Kern thinks the Bank’s estimate of spare

capacity being between 1% and 1.5% of

GDP

is reasonable.‘It could even be a shade

higher.We don’t know how much there

really is in the system. It’s hard to measure

from business surveys.’

Apart from spare capacity – which the

Bank sees as good reason to keep interest

rates low – other factors may be holding

back business investment. Hawksworth

points to the tendency, going back ten

years now, for businesses to run large

nancial surpluses rather than making

major investments.‘They prefer to retain

a strong cash position or give more back

to shareholders.’

Political uncertainty also plays its part.

Eurosceptics are expected to do well in

this year’s European elections, and the

next general election seems to promise

a government that is either less ‘business-

friendly’ or one committed to a referendum

on Britain remaining within the EU.

Neither prospect is welcomed by

international investors.

Then there is Scotland.The very

possibility of secession from the UK is

already holding up investment projects

there, according to professor Robert

E.Wright of Strathclyde Business School;

and should the ‘Yes’ vote prevail it will

be a drag on economic growth, not just

in Scotland, but across the whole of the UK.

A salient weakness in the recovery is the

continuing trade de cit and slow export

growth.‘Since the dismantling of much of

the UK’s mass-production base in the 1980s,

we’ve never managed to have an export-

led recovery,’ says professor Goodhart.

Certainly, exporters are not helped by

a strong pound, but asWood points out:

‘Sterling is still far more competitive than

before the crisis.’

Professor Goodhart notes that today’s

more specialised, high-quality exporters

are not particularly price-sensitive; and

that since UK exports are very heavily

directed towards Europe, they should

bene t from recent signs of recovery within

the eurozone.

Another perceived weakness is the UK’s

excessive reliance on services – particularly

nancial services – and regional imbalances.

But as professor Goodhart points out:‘The

trend away from manufacturing towards

services is not speci c to the UK. It’s

common among all developed economies –

with the exception of Germany.’

Hawksworth adds:‘While London

and the south-east have bounced back

quickly and are leading the recovery, other

regions have lagged behind – especially

those like Scotland, Northern Ireland and

the north-east which rely on public sector

employment more than the south-east.

However, all UK regions are now showing

some signs of recovery.’

Wood warns that the recovery is not

yet broad-based and that the current

mix of consumer and business growth is

unsustainable. He expects productivity to

pick up next year with a rise in real wages.

He also notes that ‘the structural problems

of continuing trade de cits and the chronic

lack of savings and investment remain’.The

rate of household savings has dropped from

8% to 6%, and over the longer term‘the

economy cannot grow when households are

saving less and less’.

So while he doesn’t see growth rates

returning to pre-2007 levels,Wood is

optimistic about the UK economy.‘If we

manage solid 2.5% growth over 20 years

that will make us much more a uent.’

Balance sheet

With credit flowing, house prices on

the rise and unemployment coming down, the UK

economy is surging ahead. But is the recovery sustainable

and what measures need to be taken to avoid a repeat

of the fiscal troubles of 2008?

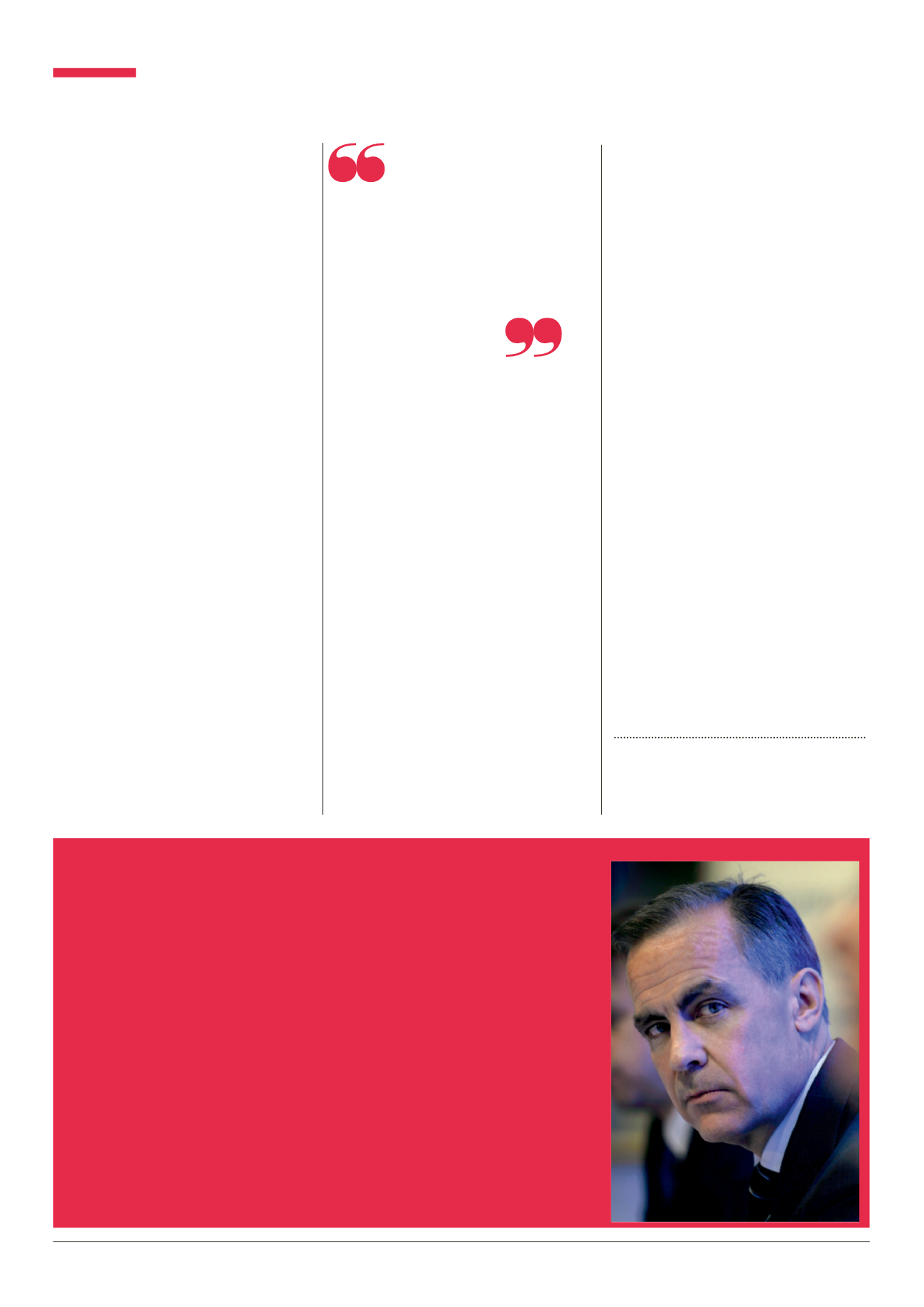

FORWARD THINKING

On becoming governor of the Bank of England, Mark

Carney (right) set out a policy of forward guidance on

interest rates intended to give markets and businesses

greater confidence.The key indicator was unemployment:

when this dropped to 7% the Bank would consider

raising the base rate.

Since then, UK unemployment has fallen faster

than expected to near that trigger point. Unwilling to

raise interest rates too soon and choke off the fragile

recovery, Carney has changed the focus of forward

guidance to indicate that rates will change when factors

like spare capacity and estimates of future productivity are

showing signs of improvement. Some critics claim this

change of tack has damaged the Bank’s credibility.

‘I always thought forward guidance was a bigger

success among businesses than it was with City

analysts,’ said Kern. ‘Carney has always said that the

Bank would keep interest rates as low as possible for

as long as possible. Businesses expect him to do that,

though it is worrying that some influential voices are

calling for an earlier rise.’

Professor Goodhart adds: ‘The Bank’s underlying

message is clear: no rise in the immediate future, and

when rates are raised it will be done slowly.’

The other key factor in deciding interest rates is inflation

which, for the first time since the crisis, has fallen below

the Bank’s 2% target. Hawksworth believes that ‘in the

short term, inflation could go even lower’.

So when will rates rise? ‘We think interest rates will start

going up in the first quarter of 2015,’ saidWood, rising

thereafter by a quarter of a percentage point every three

months or so, to between 2% and 2.5% by early 2017.

Kern anticipates no rise until later in 2015. ‘If there’s

strong growth in the economy, that’s not an issue.’ He

then expects rates to be raised gradually, as their profile

over time is equally important.

The basic message is no change until the recovery is

firmly established, though there are dangers in this. ‘The

longer interest rates are held at rock bottom the faster

rises will come,’ saidWood.

At some point, a return to normalcy is necessary.

Hawksworth warned: ‘We need a higher savings rate in

the UK, so the Bank should aim to move interest rates

gradually back to more normal levels by, say, 2020.’