38 / 40

38 / 40

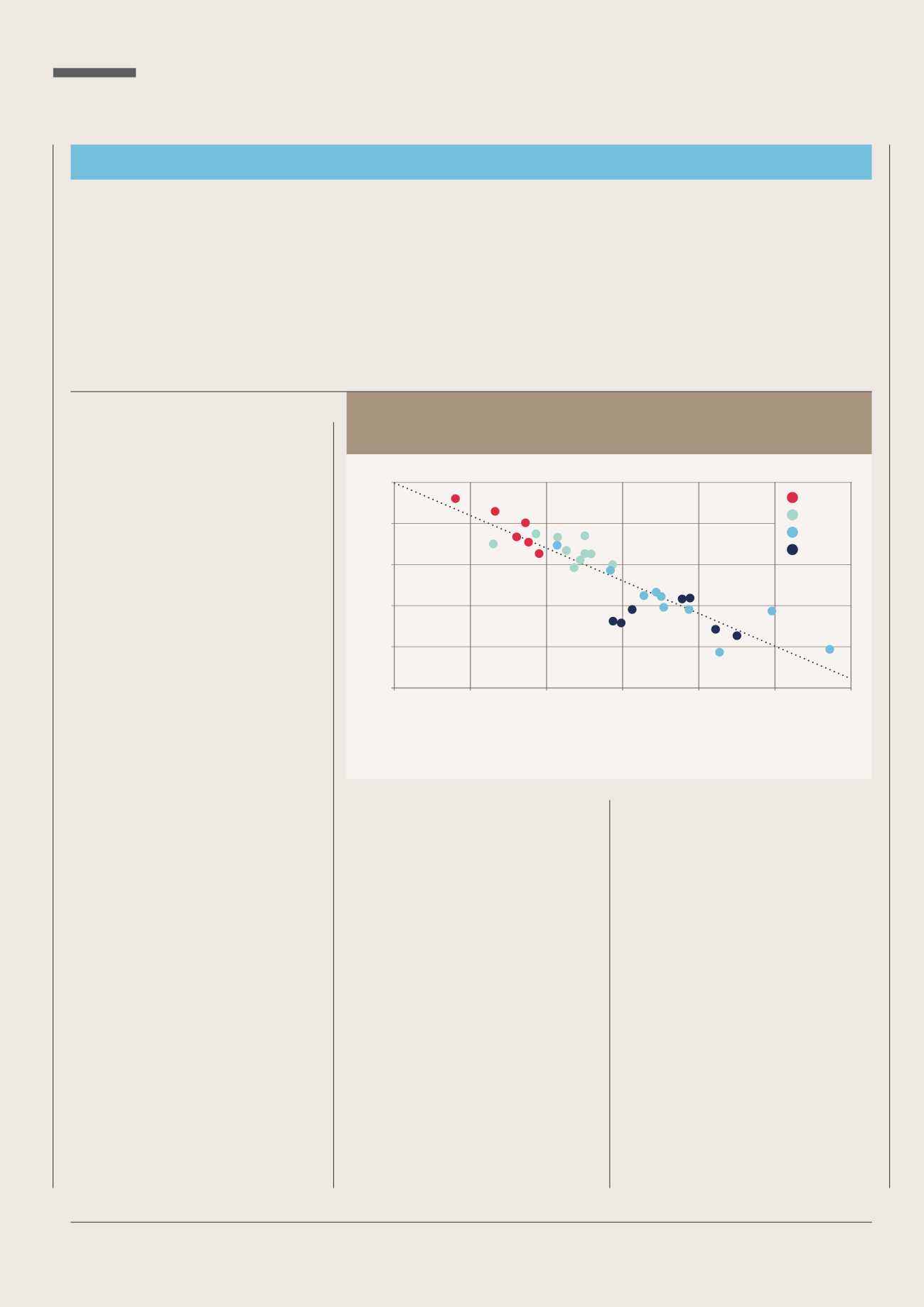

per annum over the following 10 years.

On the other hand, if an investor buys

when the market is expensive, prospective

returns can be significantly lower.At

the end of the 1990s, with the UK stock

market gripped by the dotcom bubble,

a P/E of 28 meant negative real returns

for investors over the following decade.

While there is no guarantee that future

returns will mirror this trend, the chart

suggests that the relationship between

starting valuation and subsequent

long-term returns is close. Interestingly,

the correlation is nowhere near as strong

over shorter time periods,when valuation

and fundamentals can be irrelevant;

a further reason to take a long-term

investment approach.

‘As the chart demonstrates,UK

INSIGHTS

38

|

THE INVESTOR

Research shows that starting valuations continue to be an

important indicator of long-term stock market returns

THE INVESTOR CENTRE

D

oes starting

valuation matter? It

is a question that is

often debated

among investors.

One of the key

variables investors use to determine

valuation is the price/earnings (P/E)

ratio.This is the ratio of a company’s

share price to its earnings per share.

In simple terms, a lower ratio indicates

better value.

The chart opposite shows the starting

valuation of the UK stock market, in

terms of its P/E ratio, at the end of

every year since 1974.This is plotted

against the real annualised total return

that investors would have received over

the following decade if they had invested

at that point.

A key feature of the chart is the

diagonal trend line, which shows the

relatively strong correlation between the

percentage returns and the P/E at the

time of investment.A high P/E means

that investors must pay more for every

pound of company earnings (although

the level of earnings may, of course,

change once they own the stock).

A lower multiple means they are paying

less for those earnings.

For those who invest in the market

when its valuation is low, as it was in the

1970s and early 1980s, the prospective

returns can be very attractive indeed.

Investing at the end of 1974, for instance,

resulted in a real average return of 18%

Pricepower

equities are poised to deliver attractive

long-term returns from here, but it is as

essential as ever to be selective,’ says Neil

Woodford ofWoodford Investment

Management.‘Even in the dotcom

bubble, there were cheap stocks.Active

managers made attractive returns, even

though the broader UK stock market

stagnated for the best part of a decade.’

So what does this mean for today’s

investors? TheUK stockmarket’s current

P/E of about 15 times this year’s

anticipated earnings implies a real

annualised total return of around 8%

over the next 10 years, based on the

historic trend shown on the chart.

‘This isn’t bad, especially when

compared to the likely returns from

other asset classes,’ saysWoodford.

EQUITY STARTING VALUATIONS HAVE A STRONG

INFLUENCE ON LONG-TERM RETURNS

1

Source: 1 The Lazarus Partnership,Woodford, based on FTSE All Share total return data in UK sterling, adjusted for CPI inflation

10 year real annualised total returns (%)

Price / Earnings ratio at start of period

-5

0

5

10

15

20

25

30

0

5

10

1970s

1980s

1990s

2000s

15

20

Please be aware that past performance is not indicative of future performance. Equities do not include the security of capital

characteristic of a deposit with a bank or building society.