27 / 40

27 / 40

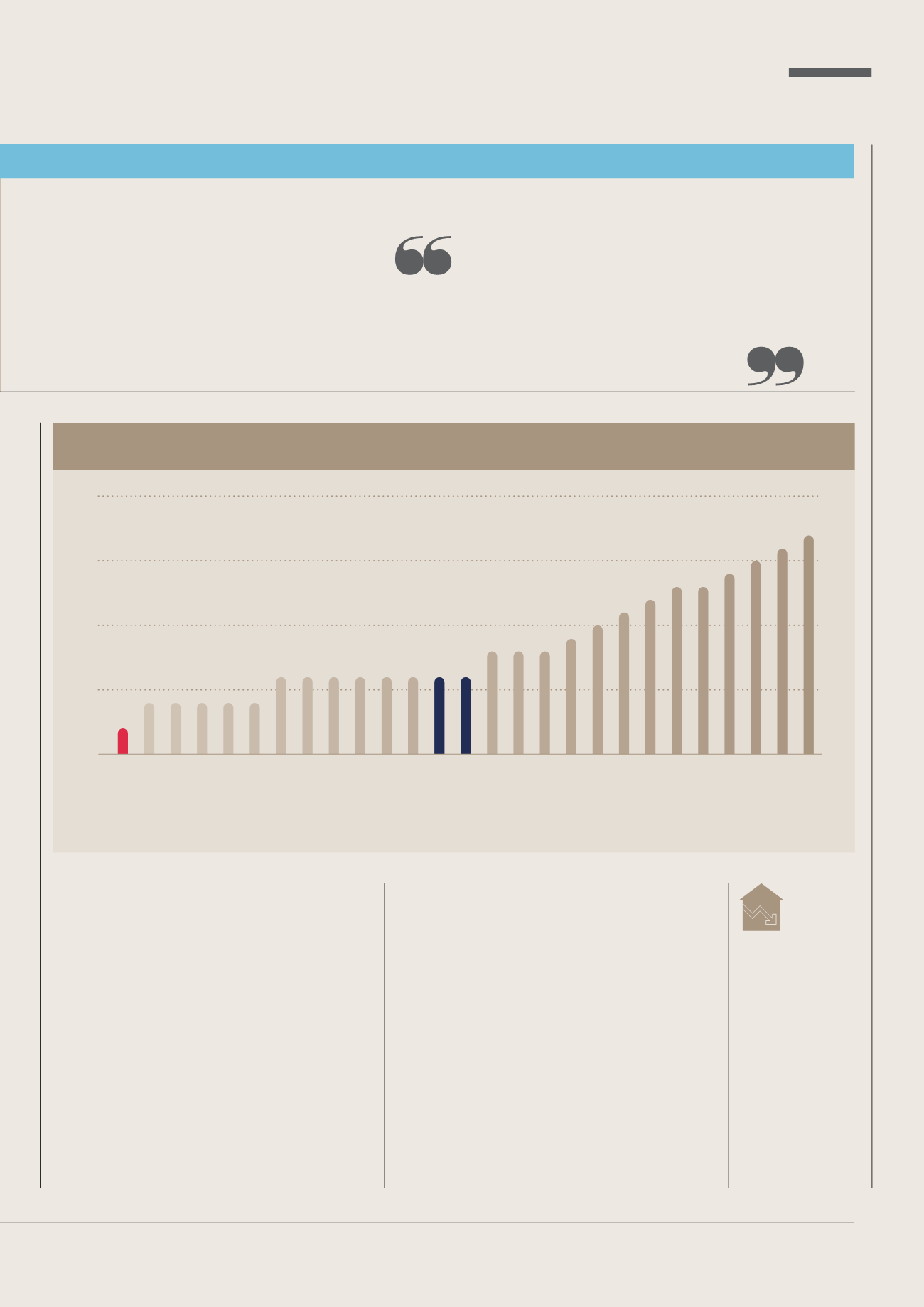

GDP growth rates in first quarter (figures published July 2017

1

)

% change over the previous quarter

The Federal Reserve plotted a more determined

course, raising rates by a quarter point and forecasting

a further rise later in the year. In fact, US in ation

had once more dipped just below 2%by quarter end,

and rst quarter GDP growth was disappointing,

while consumption fell to an eight-year low.

The S&P 500 ended the quarter up 2.7%, aided

by buoyant corporate earnings.Moreover, theVIX

(which measures volatility) refused to depart from

its extended lows for long, despite political tensions

over the FBI, climate change and trade with China.

The corporate outlook also looked bright in

Japan, where business con dence struck a three-year

high, pushing the Nikkei 225 up by more than 5%.

In the eurozone,meanwhile, the growth rate

THE INVESTOR

|

27

THE QUARTERLY REPORT

Masao Yamazaki. Sources: 1 ec.europa.eu, July 2017; 2 ons.gov.uk/economy, June 2017

The UK

household

savings rate

slipped to a

50-year

low

Ireland, Luxembourg and Malta: data not available for first quarter 2017.

*EA19: the 19 countries of the Euro area from 1.1.2015 **EA28: the 28 member states of the EU at 1.7.2013

overtook that of the US and UK, unemployment

dipped to an eight-year low and business con dence

maintained at an extended high. Structural tailwinds

surely helped, but so too did the election victories of

Emmanuel Macron, France’s new centrist,

Europhile president. French stocks rose quickly,

although the broader Euro rst 300 gained by just

1.1% over the period. In late June,Mario Draghi

indicated that the ECB’s quantitative easing

programme might soon begin to taper.

Meanwhile, EU exit talks formally began and the

UK quickly dropped its former objections to EU

‘sequencing’ in negotiations.As the quarter ended,

there were signs that business would henceforth

enjoy a louder voice in Downing Street.

United Kingdom

Greece

France

Italy

Netherlands

Sweden

Belgium

Denmark

Germany

Croatia

Cyprus

Estonia

Spain

Slovakia

Bulgaria

Portugal

Poland

Finland

Czech Republic

Hungary

Lithuania

Slovenia

Latvia

Romania

Austria

*EA19

**EU28

0.0

0.5

1.0

1.5

2.0

As the quarter ended, there were signs

that business would henceforth enjoy

a louder voice in Downing Street