06

|

THE INVESTOR

ANALYSIS

GENERAL ELECTION

Must try harder or top of the class?With the general election a matter

of months away, we assess the term of the coalition government

By David Smith

DEFICIT AND DEBT

The Conservative/Lib Dem coalition made deficit reduction a priority. In his

first ‘emergency’ Budget in June 2010, George Osborne set two targets:

to eliminate the so-called ‘structural current budget deficit’ by the end of

the parliament and to have debt falling as a percentage of GDP. Both were

supposed to be achieved by the 2015/16 fiscal year. How has he done?

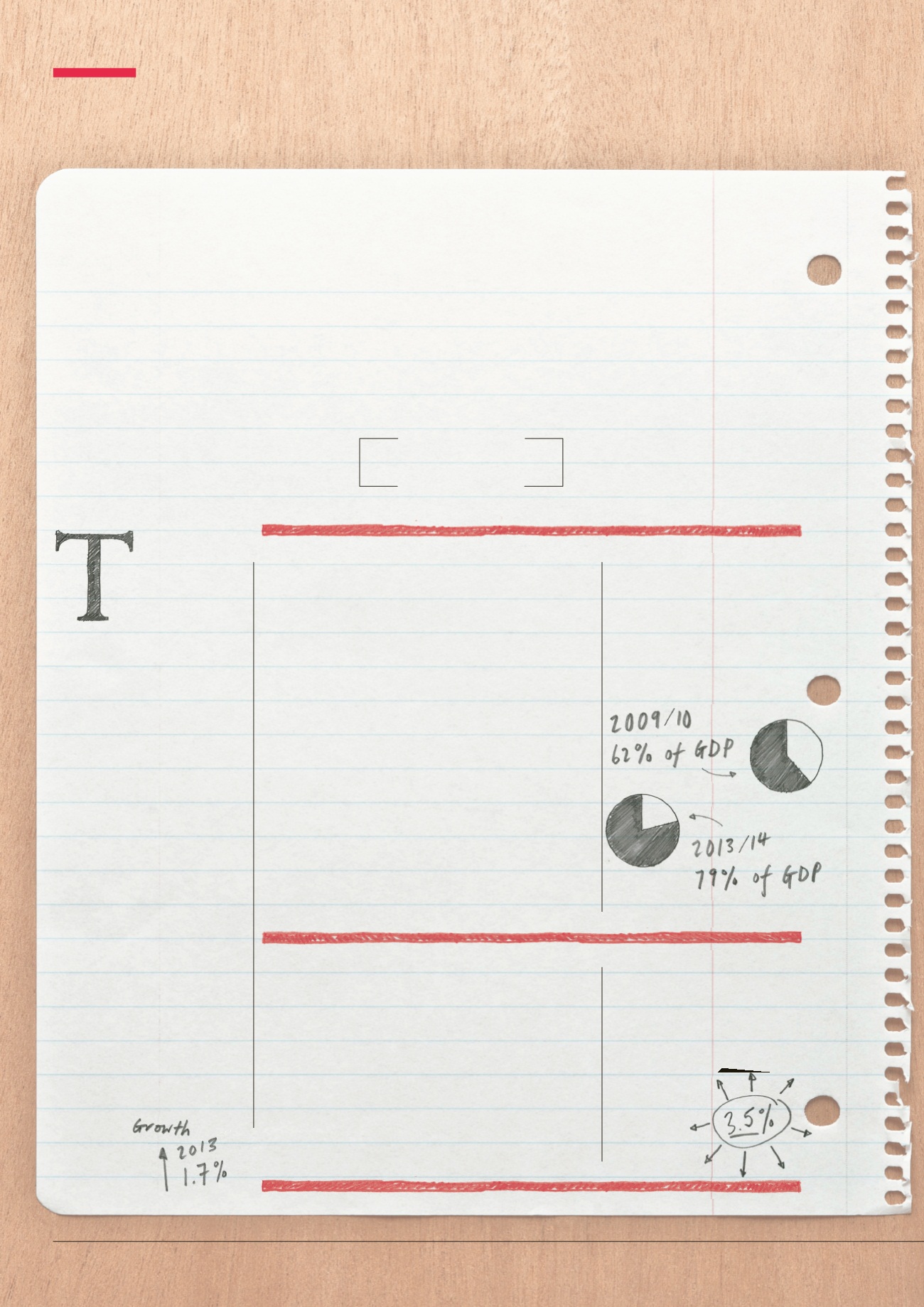

On the official measure used for the overall budget deficit, public sector

net borrowing, excluding the state-owned banks, fell from £153 billion in

2009/10 to £97.5 billion in 2013/14. The Office for Budget Responsibility

(OBR) predicts £91.3 billion for this year. In the original 2010 plan, the

deficit was intended to be £60 billion in 2013/14 and £37 billion in

2014/15. Public sector net debt rose from £956 billion at the end of the

2009/10 fiscal year, 62% of GDP, to £1,402 billion at the end of 2013/14,

79% of GDP. In late 2014 it was just over £1,450 billion.

On the two measures targeted by Osborne, the cyclically adjusted

current budget deficit and public sector net debt, there has been some

slippage. The former was supposed to have been eliminated by 2015/16

and the latter on a declining trend in relation to GDP. The latest OBR

assessment is that there will be a cyclically adjusted current deficit of 2.2%

of GDP, £41.5 billion, in 2015/16, and that it will not be eliminated until

2017/18. Public sector net debt will peak at 81.1% of GDP in 2015/16,

higher than planned, and begin to fall in 2016/17.

- -

he general

election in May

2015 is one of

the hardest to

predict for many

years.The two main parties

are broadly neck and neck in

the polls.The rise of the UK

Independence Party and the

aftermath of the independence

vote in Scotland, which has

sparked a surge in the popularity

of the Scottish National Party,

add to the uncertainty.Another

coalition – rather a curiosity in

2010 – may be the outcome.

One thing we know will play a

big part in the result will be the

performance of the economy

since May 2010. Does the

government have a record it can

be proud of, and how much is

there still left to do?

SCORECARD RESULT

There has been a considerable

reduction in the budget deficit,

which the coalition will trumpet.

But the original aim of dealing

with the deficit problem during this

parliament has not been achieved.

GROWTH

The Bank of England, in its November 2014 Inflation Report, predicted the

economy to grow by 3.5% in 2014, and by 2.9% in 2015.This suggests

a good rate at the time of the election. It has not, however, all been plain

sailing. Figures from the Office for National Statistics show that the coalition

has presided over three years in which the economy grew more slowly than

in 2010, the year it took office. Growth of 1.9% in 2010 was followed by

1.6% in 2011, 0.7% in 2012 and 1.7% in 2013.

Treasury ministers say that the weaker growth in the period from 2011

to 2013 was due to the impact of the crisis in the eurozone and high,

commodity-driven inflation. Labour says that the period of ‘flatlining’ was

because of the government’s austerity policies.

SCORECARD RESULT

Growth has come through strongly

in the run-up to the election, but

for much of the parliament the

coalition has presided over a very

weak recovery. There is ammunition

here for both the government and

its opponents.