8 / 44

8 / 44

08

|

THE INVESTOR

ANALYSIS

rising – and in some cases securing a

competitive devaluation – has been part of

the motivation for the negative rates

set by the ECB and the central banks of

Switzerland and Japan. Clearly, not

everyone could achieve a lower value

for their currency if all were to adopt

negative rates, but those who act quickly

can steal a march on others.

Are negative rates here to stay? If so,

howmuch further can they fall?While the

experiment has yet to play out, there is

a limit to howmuch longer rates can drop

or remain in negative territory. Before his

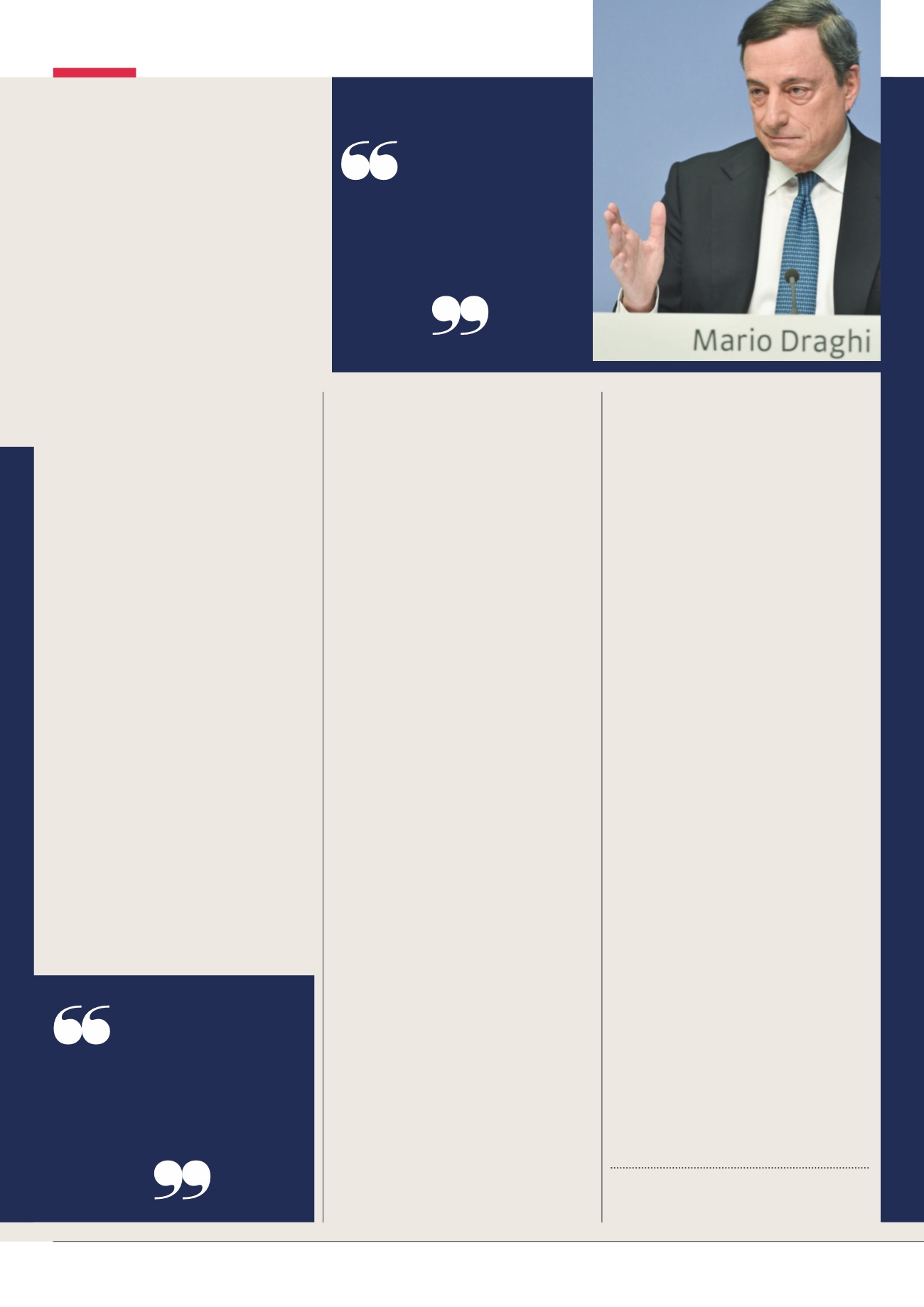

move in March, the ECB’s Draghi was

warned by the banks that his policy was

hurting them, and that any further

reduction in the rate would do damage.

After announcing another small cut he

offered broad hints that the process would

not go much further.

At the ECB’s conference following the

rate cut in March, Draghi said:‘How low

can we go? Rates will stay low, very low, for

a long period of time. Let me also add that

the experience we’ve had with negative

rates, in our case at least, has been very

positive in easing financing conditions, and

in the transmission of these better

financing conditions to the real economy.’

There is, in addition, serious resistance

to setting negative interest rates at other

central banks.The Federal Reserve in

America embarked on a process of raising

rates late in 2015, while Bank of England

Governor Mark Carney warned in a

speech in February that using negative

interest rates to achieve a lower currency

was‘a zero sum game’.The risk, he said,

Balance sheet

Central banks are using negative

interest rates to encourage the banks to lend, but the

downside could see customers close their accounts.

was of creating what he described as‘a

global liquidity trap’, in which the actions

of central banks lose any force.There was,

he said,‘no free lunch’ for central banks

in negative rates.Only time will tell

whether circumstances will force him

to change his view.

Up to now, negative interest rates have

operated in the rarefied zone of central

banks, and in their dealings with

commercial banks and the money markets.

But howwould ordinary savers respond to

negative rates; to their money being worth

less in a year’s time than it is now? It is not

as far-fetched as it sounds. In recent years,

savers have been happy to keep their

money in the bank – earning a return

barely above zero – even when inflation has

been much higher. Negative real interest

rates have been the post-crisis norm.

People are also happy to pay a monthly fee

– ostensibly for bundled products – on

current accounts, which in many cases

equates to a negative interest rate.

Both are, however, different

psychologically to an explicit negative

rate; a savings regime that would see the

value of your money, in purely cash terms,

decline year after year. Howwould people

react?We can guess, or we can draw on

research carried out recently by ING, the

Dutch-based international bank. ING

surveyed 13,000 people,mainly in Europe

but also in the US andAustralia.

The results suggest that if policymakers

think that individuals would respond to

negative interest rates by spending more

and thereby boosting the economy, they

are probably wrong. Further, negative

rates would be very bad for the banks.

As Mark Cliffe, ING’s Chief Economist,

puts it:‘A remarkable 77% said that they

would take money out of their savings

accounts.While a fewwould spend more,

this would be offset by almost as many

saving more.Most said that they would

either switch into riskier investments or

hoard cash “in a safe place”.This is better

news for safe-makers than it is for banks

and central banks.’

The most surprising aspect of ING’s

findings was not that negative interest rates

would be of limited value in boosting

spending.After all, savers still need to

put money away for a rainy day, a house

deposit or some other future need. It was

that so many would regard it as a reason

to desert their banks. So for the banks,

an experiment with negative rates for

ordinary customers could prove to be very

difficult, if not disastrous.

‘The banks would be faced with an

uncomfortable choice between not

cutting retail rates below zero, and so

seeing their profit margins squeezed, or

doing so and risking a substantial deposit

outflow,’ says Cliffe.

Negative interest rates are in fashion

among central banks. However, even

among them, there is some disquiet.There

would be even more disquiet if ordinary

savers were expected to pay banks for the

privilege of keeping their money safe.

Fortunately, that is unlikely to happen.

1

www.ecb.europa.eu, 2016

The experiencewe’ve

hadwith negative

rates, in our case at

least, has been very

positive

There is a limit to

howmuch longer

rates can drop or

remain in negative

territory