7 / 44

7 / 44

ANALYSIS

couple of UK housebuilders and Lloyds

Bank. It would be foolish to think that these

can be wholly una ected by recent – and

future – events. But with the economy

staying out of recession, as we think it

will, the impact will be limited. Lloyds, in

particular, is an interesting case – slower

credit demand and a rise in non-performing

loans will, naturally, not be helpful, but it

remains one of the world’s best capitalised

banks.Wehave regarded it as being

incorrectly valued for some time now,

and we still do. It deserves to be more

highly rated.

We have been spending time talking

with politicians and negotiators from the

European Commission and sources close

to the German government.While the

outlines of an exit agreement are as yet

very unclear (and will remain so for a good

while) it is well recognised that it would

serve no one on either side to put up trade

barriers.The UK is an important market

for larger multinationals such as Essilor and

Volkswagen, and they want to be able to

sell into the UK. Such a benign outcome

cannot, of course, be taken for granted, but

we doubt that we are wrong on this, even

if – once more – it takes time for us to be

proven right.

We will carry on doing what we have

been doing for the past 30 years – going

on the road to visit companies, carrying

out diligent research and trying to nd

new and interesting investment ideas.Our

experience of these past three decades –

which has included the invasion of Kuwait,

the second Gulf War, the dotcom crash

and the great nancial crisis of 2007 – is

that there is opportunity to be found amid

chaos.The opportunity to make money for

our investors has not gone away.

THE INVESTOR

|

07

I

t was not the result we wanted.

Nor was it the one we expected.

Nonetheless,we feel it would be

quite wrong to respond to the

Brexit vote by trying to recast our

investment stance.This is because we see its

implications as less than might be expected,

and the changes that come about will take

far longer to work through than many

commentators think. If ever there was a

time to keep calm and carry on, this is it.

Of course, it is more than likely that the

UK economy will, in the short term, grow

at a slower rate than had been expected. But

not necessarily by very much.The bu ering

impact on activity supplied by the quick

post-referendum downward adjustment

in the level of sterling should not be

underestimated.Atworst,we think growth

could be at by the start of next year;more

likely, it will still be mildly positive.

Another reason to be wary of making

big and quick changes is that the majority of

the portfolio is made up of great, super-

quality growth companies based in Europe.

Just 7% of Europe’s exports go to the

UK, and these companies will be even less

a ected by any softening in the UK than this

already low gure implies.Thinking longer

term, it remains an observable fact that

Europe has more than its fair share of great

companies.These are often companies with

great technologies and a vibrant culture

of innovation,well capable of addressing

global markets which continue to grow,

markets which are wholly una ected

by Brexit and its fallout.They include

companies such as SAP, Essilor,Amadeus

andAssaAbloy, all present in the portfolio.

We do hold, in the Greater European

Progressive portfolio, a small number of

UK-orientated companies, including a

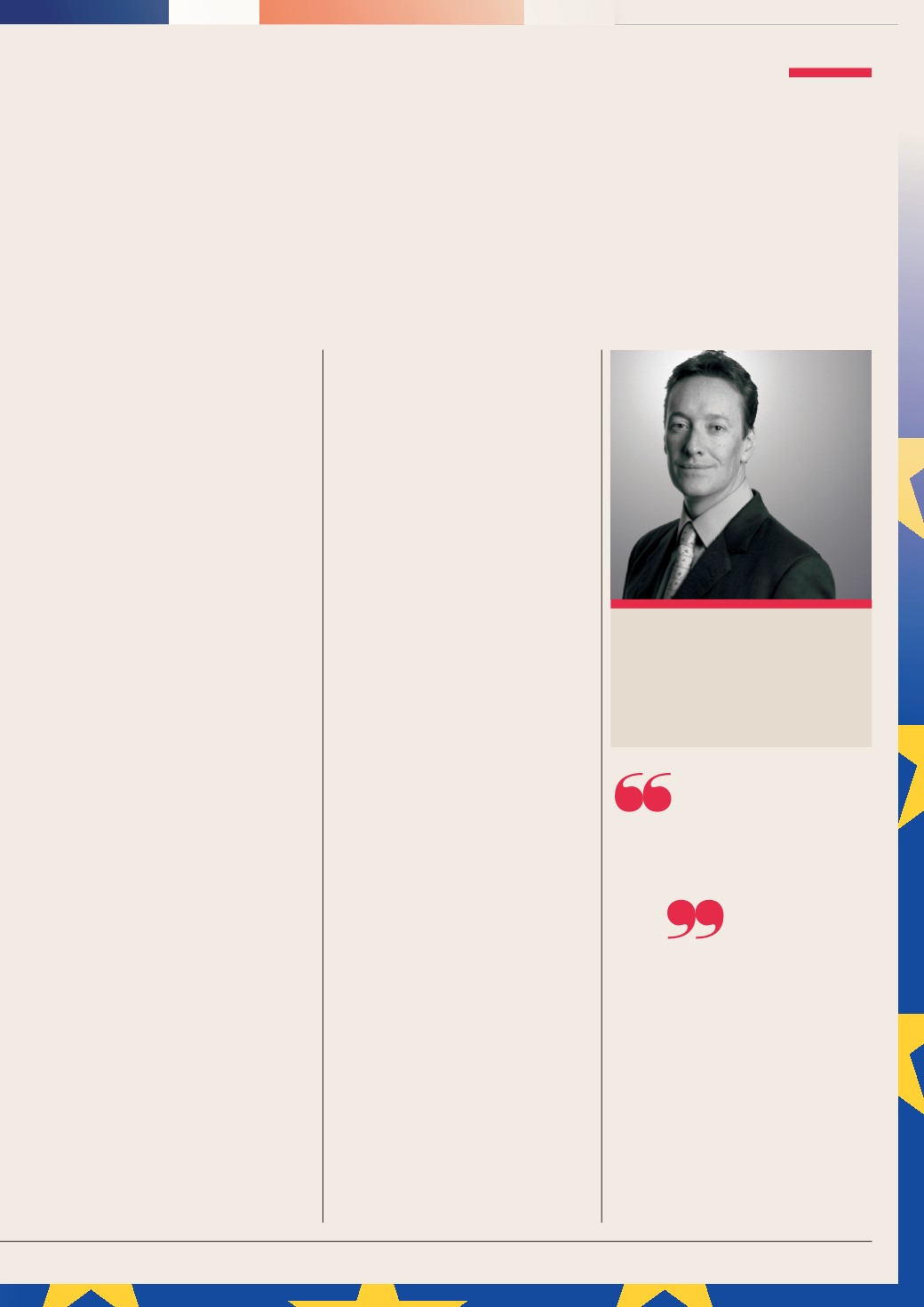

Stuart Mitchell

Continental European

and Joint Manager,

Greater European and Greater

European Progressive

At worst, we think

growthwill be flat

by the start of next

year

BREXIT

Matthew Stylianou