18 / 40

18 / 40

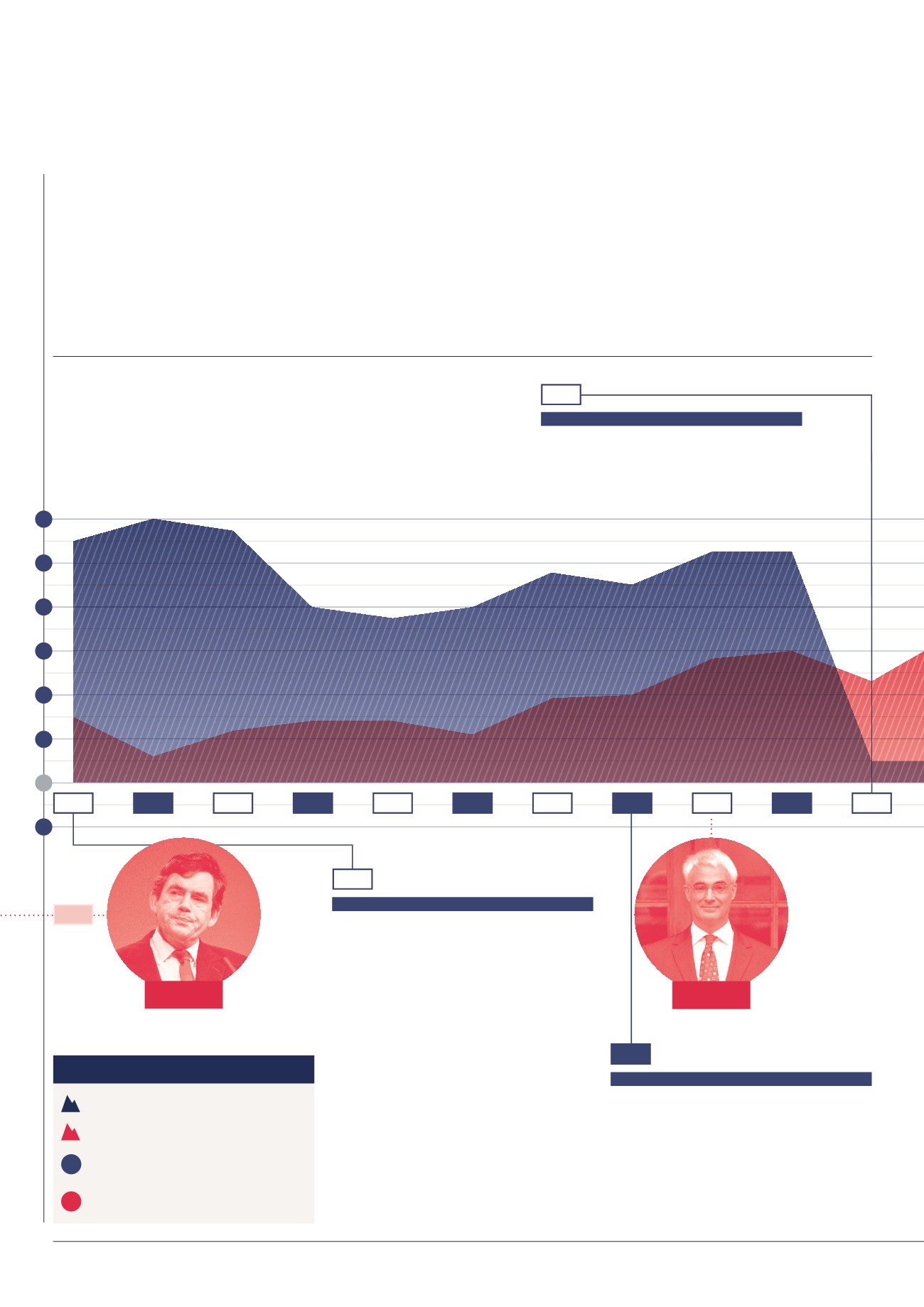

ISAs have changed signi cantly since their introduction

in 1999, both in terms of increasing investment limits

and the range of options available to investors and

savers.We chart the development of ISAs and illustrate

the struggle for real returns faced by savers choosing

the cash route.

18

|

THE INVESTOR

Eighteen years after their launch,ISAs (Individual SavingsAccounts) are one of the UK’s

most popular ways to save,but are all savers making the most of the tax advantages on o er?

The ISA debuts in the Budget of Labour

Chancellor Gordon Brown. It replaces the

Personal Equity Plans (PEPs) and Tax-Exempt

Special Savings Accounts (TESSAs), which were

introduced by the previous government to

encourage everyone to save and invest.

Contributions are made from taxed income

but investment growth and interest or

income earned in the ISA is free of Income

Tax and Capital Gains Tax. Three types of ISA

are introduced:

Cash, Stocks & Shares

, and

Insurance (but the latter was scrapped in 2005).

From the outset ISAs prove popular and

9.2 million accounts are opened in the first tax

year

1

. The overall limit is £7,000, with the Cash

ISA ceiling set at £3,000.

ISAs ARE HERE TO STAY

ISA ALLOWANCE INCREASES

BIRTH OF THE ISA

2006

ISAs at18

1999

2009

1999

1997

2009

2004

2000

2005

2001

2006

2002

2007

2003

2008

1

-1

2

3

4

5

6

Ed Balls, Economic Secretary to the Treasury,

announces that ISAs will have a permanent

future. He also announces a big shake-up to

the ISA regime: until now, savers were not

allowed to switch money from a Cash ISA

accrued in a previous tax year into a Stocks

& Shares account.

Chancellor Gordon Brown raises the ISA limit to

£10,200, of which £5,100 can be held in cash. At

first, only the over-50s benefit.

Alistair

Darling

Gordon

Brown

Chancellor of the Exchequer

(Labour)

INTEREST RATES

V

INFLATION

Inflation (CPI)

Bank of England base rate

Chancellor of the Exchequer

(Conservative)

0