13 / 44

13 / 44

THE INVESTOR

|

13

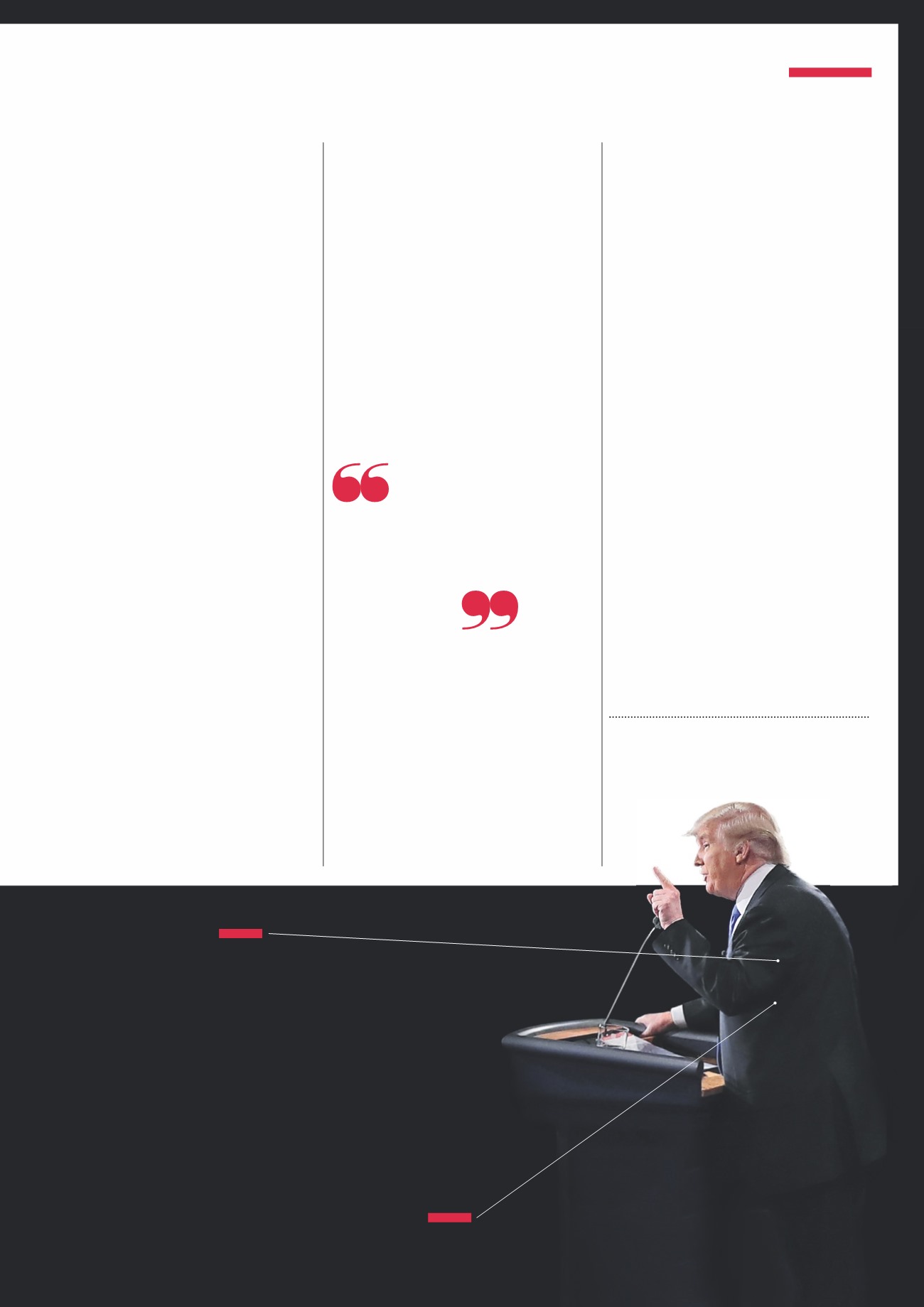

Proposed new

top rate of tax at

33

%

on incomes above

$154,000

a year

1

Pledged

to reduce

corporation

tax to

15

%

1

1 bbc.co.uk, September 2016. 2 hillaryclinton.com

RonaldReagan’s second victory,shares rose

by 26% the following year, there has only

been one bad year following a presidential

election; the 13% fall in the markets in

2001 that came after GeorgeWBush’s first

success in 2000.Both theObama wins were

followed by big stock-market gains; 23% in

2009, and an even more impressive 30%

four years

later.Incontrast,four presidential

elections from 1968 to 1980 were followed

by significant losses the following year

1

.

John Higgins, an analyst with Capital

Economics, suggests this tells us more

about prevailing economic conditions than

market approval or disapproval for the

election outcome. So the solitary bad

post-election year in recent times, 2001,

mainly reflected the bursting of the

dotcom bubble and the 9/11 attacks on

America.The big gains of 2009 were less a

vote of confidence in Obama than a

rebound from the market crash of 2008.

‘We are not forecasting an imminent

recession in the US and do not consider that

its stock market is particularly overvalued,’

said Higgins.‘We doubt that the outcome

of the election will send equity prices into

a tailspin,whatever the result.’

The other possible source of reassurance

is the US Federal Reserve.Trump accused

the Fed of favouring his opponent by not

raising interest rates in election year. Janet

Yellen, the Fed Chairman, has though

made it clear that a rate hike in December

is on the cards.That could also be delayed if

the election result is viewed by the Fed as

destabilising.Inanother echo of the Brexit

vote,the resultmaymatter less to themarkets

than its implications for the bank rate.

That said, this is a highly unusual election.

Never before in modern times have

investors had to assess the implications of a

candidate from so far outside the political

mainstream. Nor has it been easy to pin

down theTrump policy agenda.There are,

however, clear differences between him and

Clinton. She would raise taxes on the very

highest paid,with a new 43.6% tax bracket

on incomes above $5million a year, up from

39.6

%now.He, in contrast,would bring

down the top rate of tax to 33%.Under

Trump, that new top rate would kick in at

$154

,000.Hehas also pledged to reduce the

corporation tax rate from35% to just 15%.

The effects on the US budget deficit could

be dramatic.The independentTax Policy

Center calculates Trump’s programmewould

reduce tax revenues by $9,500 billion over

a decade (theTrump camp admits to less

than half of that amount), while Clinton’s

would boost them by $1,100 billion

2

.

Even more striking are the differences

on trade policy.While Clinton has wobbled

on trade,Trump has been explicitly

protectionist. Clinton has stated that the

Trans-Pacific Partnership (TPP), the

Asia-Pacific trade deal negotiated under

Obama, is not the best deal for the US.

Trump, however, with his proposal for a

35% tariff on imports fromMexico and

one of 45% on imports fromChina, would

– if he carried out his threats – fire the

opening shots in a new and potentially

dangerous trade war.

ATrump presidency, coming when

world trade is weak anyway – theWorld

Trade Organization estimates world trade

growth of under 2% this year

3

, the weakest

since the global financial crisis – could

plunge the world into a new protectionist

age. Even if his bark is worse than his bite,

and even if the checks and balances of the

US political system prevent him from

doing all he says he wants, that may be

something for investors to think about.

Trump’s tax policy

would reduce revenues,

while Clinton’swould

boost them

1 Capital Economics, September 2016

2

bbc.co.uk,September 2016

3

wto.org, September 2016

Balance sheet

The markets would seem to prefer

a Clinton victory; the prospect of Trump occupying

the White House brings uncertainty. Either way, a US

recession is not considered a likely outcome.

2016 US PRESIDENTIAL ELECTION

ANALYSIS